The most lively pie fight on the political blogosphere the past two days is over the forecast of the effect of Bernie Sanders’ economic policies by University of Massachusetts-Amherst economist Gerald Friedman. According to Friedman, if Sanders’ policies of free college education, national health care, new infrastructure spending, and increased Social Security benefits were actually implemented, the result would by a eye-popping annual GDP growth rate of 5.3 percent over ten years, with a net increase of 26 million new jobs.

Four former heads of the Council of Economic Advisers, under Presidents Clinton and Obama—Laura D’Andrea Tyson, Christina Romer, Austan Goolsbee, and Alan Krueger—posted a joint letter to Sanders and Friedman, denouncing Friedman’s study for making “extreme claims… that cannot be supported by the economic evidence.”

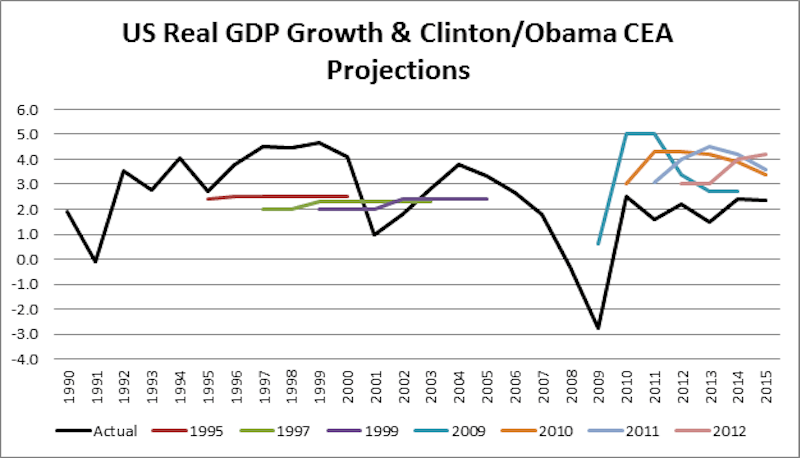

The graph below shows how successful Tyson, Romer, Goolsbee, and Krueger were at doing forecasting themselves. In two words:

NOT VERY.

That graph is taken from David Dayen’s article on today’s website of The New Republic, The Pious Attacks on Bernie Sanders’s “Fuzzy” Economics. It is a relentless smack-down of the honesty and competence of these critics.

For example, the 2010 EROP, overseen by then-Chair Christina Romer, made real GDP projections of 4.3 percent in 2011 and 2012, and 4.2 percent in 2013. This was wildly optimistic. According to Federal Reserve Economic Data, the actual real GDP growth rate in 2011 was 1.6 percent; in 2012, 2.2 percent; and in 2013, 1.5 percent.And,

Goolsbee’s claim in March 2007, after the housing bubble peaked and foreclosures began to skyrocket, that “the mortgage market has become more perfect, not more irresponsible” is perhaps one of the worst economic arguments of the past several decades.In my judgement—and I have been writing about economics since the late 1980s—Tyson, Romer, Goolsbee, and Krueger are all failures, with no professional credibility left. Sound harsh? Well, actually, I think the same about almost every professional economist these days. Recall that in October 2009, the Huffington Post revealed that over half of all professional economists in the United States have been paid by the Federal Reserve in some form or another.

Back in the presidency of Franklin Roosevelt, the Fed did not have the stranglehold on the economics profession it has now. Do you agree with Tyson, Romer, Goolsbee, and Krueger that it is outlandish to forecast 26 million new jobs in ten years? Well, try this out for size: in the winter of 1933-34, President Franklin Roosevelt’s Civil Works Administration (CWA), created over four million jobs in just one month.

Earlier today, Illinibeatle posted about David Sirota’s little exercise in journalism of tracking the sources of income for Goolsbee and Tyson. Turns out they are doing quite well, thank you very much, in their cozy positions on Wall Street.

Back in January 2008, when I assessed the economics teams of Edwards, Kucinich, Obama and Clinton (Who will tell Wall Street to shove it?), it was precisely because of Goolsbee’s position as candidate Obama’s top economic adviser that I concluded that if elected President, Obama would most likely surrender to Wall Street and fail to reverse the past four decades’ descent into economic neo-liberlaism, a.k.a. radical conservative “free market” and “free trade” economics.

Looking back at that post right now, I think I called it exactly right:

None of the candidates – Republican or Democrat – are talking about these financial crises, and the economic onslaught they portend…. the next president of the United States is going to be dealing with an economic collapse. The extreme level of economic hardship that will likely result is going to make the population more open to radical solutions…And I stand by what I forecast then:

Either we demolish the power of Wall Street and dismantle the structure of speculative finance and return to industrial capitalism and a Keynesian goal of full employment and wage growth, or the United States will cease to exist as a free, democratic republic in the next ten to twenty years… There is NO solution to these financial and economic crises within the presently accepted economic belief structure of U.S. elites.So, the question of who is an economic adviser to which candidate for President, and where that economic adviser derives a livelihood, is not only a legitimate public concern, but is a crucial measure of how fit a particular candidate is, to be the leader of the free world.

Let me suggest that there are a few questions that comprise a short test of whether a particular economic adviser is going to help lead us into further neo-liberal economic deterioration and ruin, or will be a source of ideas and advice that will help us begin to rebuild our deindustrialized and decapitalised economy so that we have the capacity to begin to build the new $359 trillion world economy needed to solve the problem of global climate change.

1) Did this economist foresee the financial crises of 2007-2008?

2) Did this economist foresee that the American Recovery and Reinvestment Act of 2009 (the “Obama Stimulus”) of $831 billion was woefully inadequate?

3) Does this economist recognize and accept the conclusions of the scientists and engineers who have “worked the numbers” on solving global climate change, that we need hundreds of trillions of dollars of new investment in clean energy and transportation systems over the next couple decades?

4) Does this economist recognize that the single most important power of the global elite straining to protect the status quo at this time, is that elite’s monopoly over the creation and allocation of money and credit?

5) Did this economist oppose NAFTA and other free trade agreements, and warn that they would create a “race to the bottom”?

The answers to these questions, in my opinion, will easily peg any particular economic adviser as competent, or incompetent.

I am pretty sure that Tyson, Romer, Goolsbee, and Krueger failed all five of these questions. But, from the amount of echo-chamber posting of their attack on Friedman’s study, there are apparently a lot of people out there, who like to think they are liberal and progressive, but who don’t have a clue about how to judge economic competence and policies.

I so wish I could follow everything you’re saying:

ReplyDelete1. “According to the economist Gerald Friedman, if Bernie Sanders’ policies (of free college education, national health care, new infrastructure spending, and increased Social Security benefits) were actually implemented, the result would be an eye-popping annual GDP growth rate of 5.3 percent over ten years, with a net increase of 26 million new jobs.” (Which sounds good to me.)

2. However, 4 top economists from the Clinton/Obama administrations dispute what the economist Gerald Friedman says, and you dispute them…which, although I can’t follow all the squiggly lines on the graph you offered I do trust your judgement that the four top economists from the Clinton/Obama administrations are all failures (which sounds about right to me so why not keep it simple)? I am not a Clinton fan but I did vote for Obama in 2008 and I regret it…that he didn’t come close to what I was hoping for so there was no way I could vote for him again or anyone else in 2012.

3. So what to do in 2016? That’s the big question: Is it simply a question of economics…or could it be something bigger than that? Will Bernie Sanders be at least a step in the right direction who if elected at least he won’t betray us like Obama did, or might he? Obama claims he wanted to do lots of good stuff but congress wouldn’t let him…so why did he stop asking? How come he didn’t call on the American people to march on government offices everywhere and show our discontent (peacefully of course)?

I don’t doubt that Tyson, Romer, Goolsbee, and Krueger are all failures (in more than just economics). And I don’t doubt that the “echo-chamber posting” of people on the internet who would “like to think they are liberal and progressive,” aren’t. So to heck with them, “Sock it to them!” I say. But please “Keep it Simple” if you can. Thank you.

PS: Would it shake things up if Joe Biden announced he would be willing to stay on as VP (to give Bernie Sanders some clout and credibility he might not enjoy any better way)? Do you think Biden was/is a true liberal/progressive like Bernie?

David Dayen discusses the difficulties of economic modeling. I did not include the fact that yesterday Joseph Stiglitz slammed Tyson, Romer, Goolsbee, and Krueger for not even doing any analysis at all! They just attacked Friedman; and I think Neil Irwin in the NY Times has it right: "something more tribal is going on." Sanders' policies are basically a slap in the face of the Democratic Party policy establishment; Sanders policies imply that the technocratic meritocracy of policy making is a failure. Of course, those who are members of that meritocracy don't like hearing that.

ReplyDeleteI voted for Obama, and evened helped campaign locally for him, even though my assessment of his economic advisers had led me to conclude it was unlikely he would actually engage Wall Street in a serious fight. The one hope I had was that the community organizer in him would come to the fore at some point. Alas, it hasn't, and he seems genuinely befuddled and annoyed when people argue his policies have failed. And that includes people on all sides of the political spectrum, because he honestly believed in bi-partisanship. That is what he practiced as editor of Harvard Law Review, and it worked there. He thought it would work while he was President, and it appears to have taken almost six years for him to realize how mistaken he was.

I wouldn't place high hopes in Sanders, though I strongly support him for the basic reason that he is leading what I consider a genuine populist insurgency from the left against the status quo and the powers that be--more of an insurgency than Obama had (and threw away). The worst thing about Sanders, of course, is his socialism. As Jon and I have repeatedly written, socialism is a failed ideology. And as Jon has written a number of times, socialists all over the world have generally sold out to neo-liberalism.

There are certain great weakness which characterize socialists and the left in general. They don't seem to understand the epistemology of classical republicanism at all. In fact, they scorn it. This blinds them to the very long-term cultural warfare the reactionaries of old Europe have waged against the USA in particular, and republican self-government in general. The fact they tolerated the development and emergence of the incredibly destructive ideology of libertarianism is proof of how defenseless they have left themselves. Jane Mayer's new book, Dark Money, is typical: she does not even mention the Mont Pelerin Society. They are also blind; nay, quite hostile, to the concepts of private and public virtue that are inextricably bound up with classical republicanism. They thus dismiss the formation of the USA as just one group of greedy old white men shouldering aside another group of greedy old white men, and thereby they abandon the Enlightenment ideals that resulted in creating the USA. It was those Enlightenment ideals that the world admired about the USA, but no longer.

I appreciate that thoughtful reply, thank you. I’m not sure what to make of the “isms.”

ReplyDeleteCapitalism (politics): A way of life that favors formation of private wealth to own and control everything...is often considered synonymous with the economic relations that (supposedly) emerge naturally to control the world in the absence of political control (but it’s a deception). When a bank or a business venture is bailed out by the government it is called “a smart business move to protect the financial well-being of the planet.” But when a person or a family is bailed out by the government it is called “entitlement fraud and creeping Socialism.” Free-market laissez-faire (capitalism) (the most celebrated form of private wealth after inheritance) will not rest until all forms of public property and public wealth are “Privatized! (Which could happen as early as this summer...or the coming election in November if we get that far.)

Socialism (politics): A form of collectivism that emphasizes public ownership of all important public assets and the means of public production...it justifies subordination of the individual to the community through democratic means (not totalitarian or authoritarian means) but it does tend to be completely unfair and unsympathetic to rich people (because it treats the rich the same as everybody else when it is obvious to the rich that they deserve more than everybody else because they can afford to buy so much more than everybody else) and that’s always been a problem.

Collectivism (politics): A doctrine that an individual's actions should benefit some kind of collective organization (such as a tribe, community, profession, or state) but, it too tends to be completely unfair and unsympathetic to rich people (unless the rich are collectively in charge).

Someone once said, “The only cure for the ills of democracy is more democracy.” And I think that’s right (or left) or true, especially when democracy requires us to talk to each other and learn things like, “The only cure for the ills of capitalism is social democracy.” Social democracy allows us to cope with the growing number of non-monetary problems we face... as our non-renewable planetary resources diminish, as our renewable resources aren’t regulated enough to make them stretch through the renewable cycle, and as our “one and only one biosphere” on our one earth continues to degrade at an alarming rate. We won’t be able to buy our way out of these problems...only our collective wits and collective actions will have a chance to cope... whether our collective hearts and minds are up to the task or not.

Dr. Peter Whybrow, MD, author of “American Mania,” (inspired by 9/11/2001) and in his latest book, “The Well-Tuned Brain, The Remedy for a Manic Society,” (inspired by our wrong-headed bailouts in 2008) he makes the case that “Our brain is a hybrid of ancient instincts with a bias toward short term goals and emotions that Trump reason,” which, on top of everything else, maybe all we can do about the rich is give them a spanking and send them to bed early without supper to ponder what they might do with their money...while there’s still time for them to do anything real and lasting (planet-wide) that might help. http://www.peterwhybrow.com/

Like maybe sponsor a world-wide symposium on the “complete” Adam Smith who recognized that human “character” (the delicate balance between pleasure-seeking and prudent self-restraint) is not born in us but crafted through thoughtful “self-command,” where each person is their own best critic... BUT that it’s also “A Social Problem with a Collective Responsibility that has been lost in the world over the past 50 years because of Extreme Modern Market Hysteria!”

Dissimilar to most money related markets, the remote trade market has no physical area and no focal trade. The Forex market works 24 hours a day through an electronic system of banks, partnerships and individual merchants. Forex exchanging starts each day in Sydney, then moves to Tokyo, trailed by London and after that New York. The significant business sector producers, or merchants, comprise of the business and speculation banks, and enlisted prospects commission shippers (FCMs, for example, FX Solutions.You need more data welcome to visit us Hot Forex Signals

ReplyDelete