My long description of why I believe the gold bugs have at best, a superficial understanding of economics and monetary policy can be found at my web site. But in brief, money has two main elements making up its worth. Either it can be exchanged for something more tangible (gasoline, food) or it can buy human talent, work, and creativity. Of course, there are other strategies a society can use to validate its currency. As the old Greenbackers used to say, any money that you can use to pay your taxes is good. And obviously any money that you can use to retire your debts has value because the lender had agreed it has value.

But even the economically conservative Atlantic felt the need in August to demonstrate yet again why even the favorite argument of the gold bugs—price stability—is not much of a talking point after all.

Why The Gold Standard Is The World's Worst Economic Idea—In Two Charts

Matthew O'Brien, The Atlantic | Aug. 26, 2012

The greatest trick Ron Paul ever pulled was convincing the world that the gold standard leads to stable prices.

Well, maybe not the world. Just the Republican Party. After a 32-year hiatus, the party's official platform will include a plank calling for a commission to look at the possible return of the gold standard. There might be worse ideas than this, but they generally involve jumping off the Brooklyn Bridge because everybody else is doing it.

Economics is often a contentious subject, but economists agree about the gold standard -- it is a barbarous relic that belongs in the dustbin of history. As University of Chicago professor Richard Thaler points out, exactly zero economists endorsed the idea in a recent poll. What makes it such an idea non grata? It prevents the central bank from fighting recessions by outsourcing monetary policy decisions to how much gold we have -- which, in turn, depends on our trade balance and on how much of the shiny rock we can dig up. When we peg the dollar to gold we have to raise interest rates when gold is scarce, regardless of the state of the economy. This policy inflexibility was the major cause of the Great Depression, as governments were forced to tighten policy at the worst possible moment. It's no coincidence that the sooner a country abandoned the gold standard, the sooner it began recovering.

Why would anyone want to go back to the bad old days? The gold standard limited central banks from printing money when economies needed central banks to print money, and limited governments from running deficits when economies needed governments to run deficits. It was a devilish device for turning recessions into depressions. The answer is that some people aren't worried about depressions. Some people are worried about inflation. Even when none exists. To them, these fetters are the feature, not a bug.

It's a simple idea. If governments can't print or spend too much money, prices should be stable. Simple, but wrong. Consider the chart below, which shows headline CPI inflation under the gold standard from June 1919 to March 1933*. Not exactly an, ahem, golden age of price stability.

The gold standard should guarantee price stability in the long run, but you know what they say about the long run -- we're all dead. In the short run, prices can change violently under the gold standard, as the balance of trade changes or the physical stock of gold changes. Remember, price stability isn't just about avoiding inflation; it's about avoiding deflation too. The gold standard wasn't good at either -- especially compared to our modern inflation-targeting system.

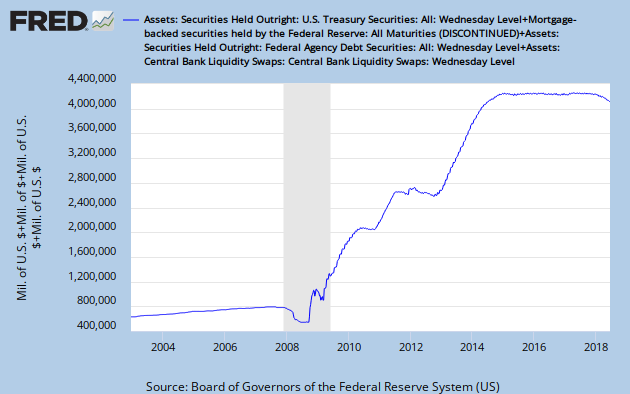

Consider the same chart of headline CPI inflation, this time since the Federal Reserve began quantitative easing in November 2008.

Now that's what stable prices look like. There's been 23 times less variance in prices since the Fed started quantitative easing than there was under the gold standard. Read that again. It's hard to understand why conservatives have been so up in arms about quantitative easing when you look at the reality. Yes, the Fed has expanded its balance sheet to unprecedented levels, but if it hadn't done that prices would probably be falling a bit now. But how will the Fed eventually mop up all this liquidity it's created -- hasn't it lit the fuse of an inflation time-bomb? No. The Fed can increase the interest it pays on reserves, do reverse repos, or use term deposit facilities to prevent banks from lending out too much money, if it comes to that.

The gold standard is a solution in search of a problem. Actually, it's worse than that. It's a problem in search of a problem. Prices would have to fall a great deal if we adopted the gold standard today. In other words, it would turn the imagined problem of price stability into a real problem of price stability. And, of course, this ensuing deflation would send the economy into a death spiral due to still high levels of household debt.

Whether it's 1896 or 2012, it doesn't make sense to crucify our economy on a cross of gold. more

{kind=link}

No comments:

Post a Comment